In the previous article, we covered how to build a stock picking algorithm without coding — the process, the tools, and what to look for in backtest results.

This article goes one level deeper: two concrete strategies with real rule setups you can replicate in AlgoCloud today.

What Makes a Good Stock Picking Strategy?

Before the examples, a quick framing. A good algorithmic stock picking strategy has three things:

- A logical reason to work — not just a pattern that happened to fit historical data

- Consistent results across market regimes — bull markets, bear markets, sideways markets

- Manageable drawdowns — losses you can actually stomach without abandoning the strategy

With that in mind, here are two approaches that check all three boxes.

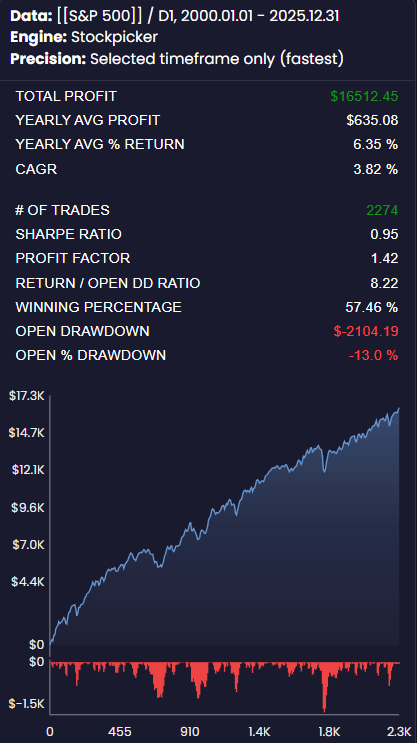

Strategy 1: Momentum Large Cap

Core idea: The best-performing large cap stocks over the past 6 months tend to keep outperforming over the next 1–3 months. Buy them systematically, rebalance regularly.

Why it works: Momentum is one of the most well-documented factors in financial research, with evidence going back over a century. It reflects the

behavioral tendency of investors to underreact to

positive news — prices continue rising as more investors catch on.

Rules in AlgoCloud

- Universe: S&P 500 stocks

- Filter: Average daily volume > 500,000 shares (liquidity)

- Ranking: 1-month price return, highest first

- Selection: Top 15 stocks

- Rebalancing: Monthly

What to expect

Strong performance in trending bull markets. Momentum strategies can suffer sharp, fast drawdowns during “momentum crashes” — sudden reversals where the best performers become the worst. These are rare but can be significant. Monthly rebalancing helps limit exposure.

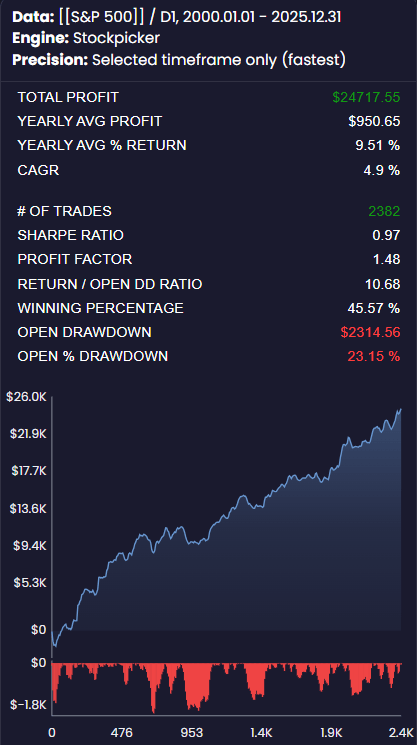

Strategy 2: Mean Reversion

Core idea: When a stock drops sharply in the short term without a fundamental reason, it tends to return to its average. Buy after the drop, sell after the recovery.

Why it works: Markets overreact — in both directions. Excessive pessimism around an individual stock creates temporary dislocations that statistically correct themselves. Mean reversion exploits this tendency systematically.

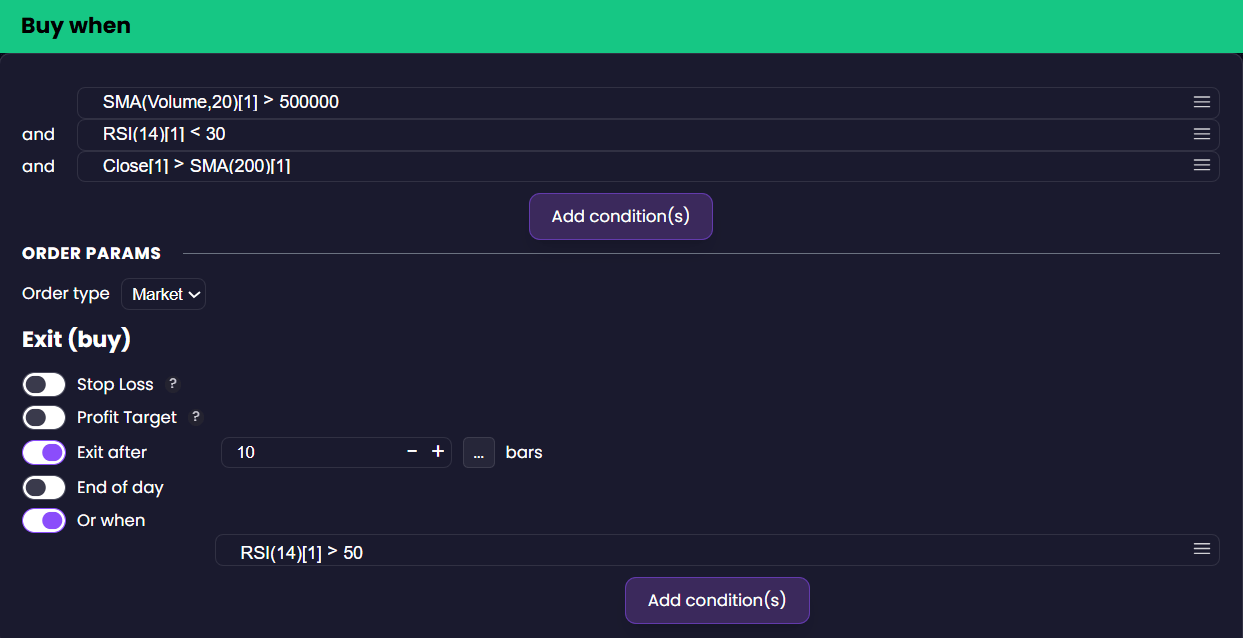

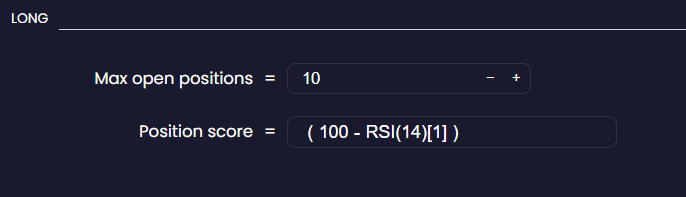

Rules in AlgoCloud

- Universe: S&P 500 stocks

- Filter: Average daily volume > 500,000 shares

- Filter: RSI (14-day) < 30 — stock is technically oversold

- Filter: Price > 200-day moving average — still in a long-term uptrend

- Selection: Top 10 stocks with lowest RSI

- Exit: Sell when RSI > 50 or after 10 days

What to expect

Mean reversion works best on stable, liquid stocks in trending markets. In strongly trending bear markets it can fail — a stock “oversold” at RSI 28 can keep falling. That’s why the long-term uptrend condition matters.

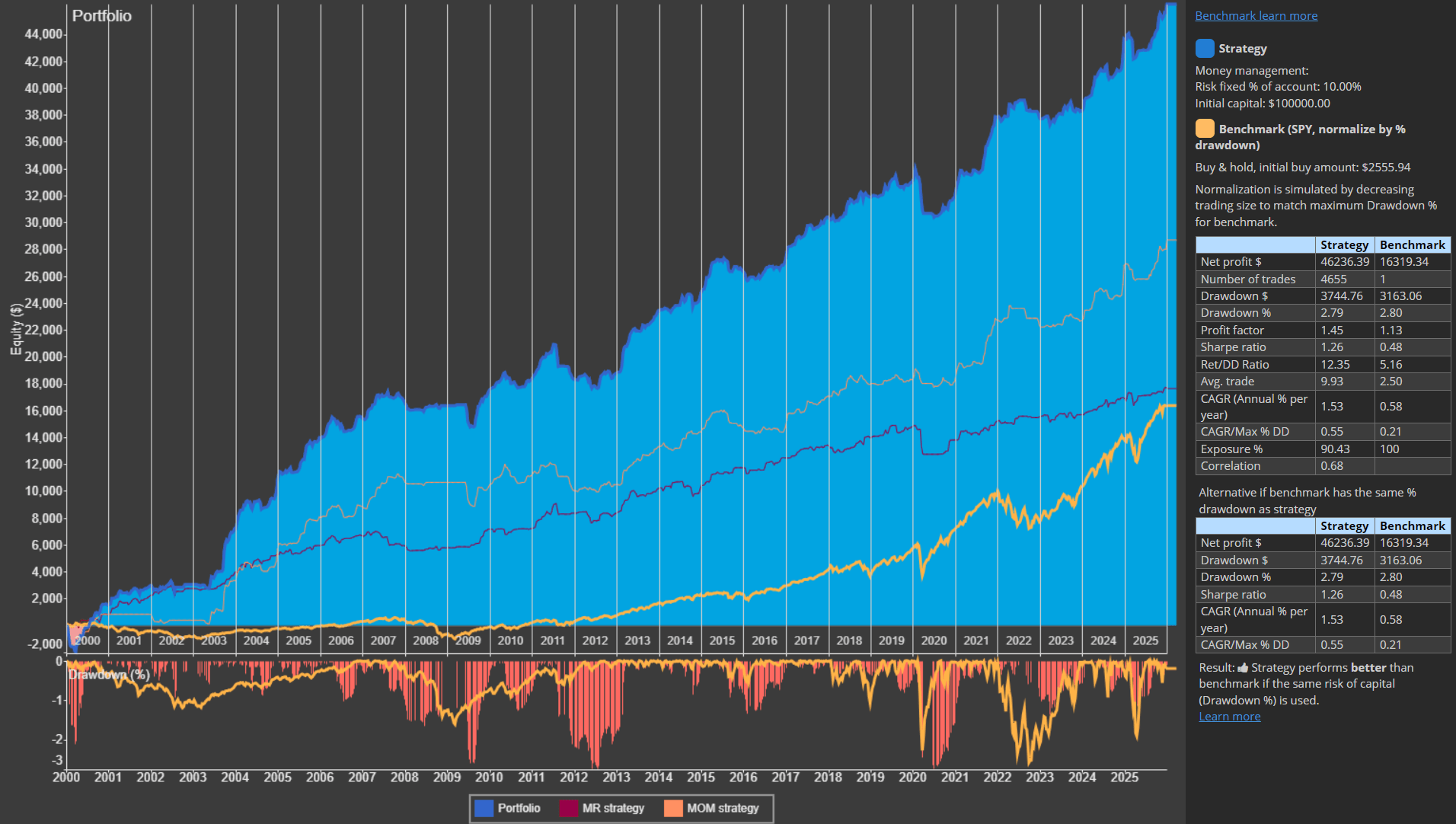

Running Both Strategies Together

Momentum and mean reversion are opposite by nature — and that’s exactly why running both makes sense.

Momentum profits in trending markets, when strong stocks keep rising. Mean reversion profits in sideways or volatile markets, when stocks oscillate around their average. The combination means the portfolio works across more market conditions, not just one.

Both strategies can run simultaneously in AlgoCloud, each with its own position sizing and schedule.

Common Mistakes to Avoid

Over-optimizing the rules. If you spend hours tweaking parameters until the backtest looks perfect, you’ve memorized the past rather than found a real edge. Define the logic first, then test.

Ignoring transaction costs. For stocks, costs are low — commissions are fractions of a percent, and Alpaca trades commission-free. Still, for strategies with high trade frequency, costs add up. Include them in your backtest so results reflect reality. For a deeper look at real-world trading costs, see our analysis of actual transaction costs.

Testing on too short a period. Five years of data isn’t enough. It might cover only one market regime. Test on at least 15–20 years — AlgoCloud gives you 30+.

Frequently Asked Questions

Can I run both strategies at the same time?

Yes. Running multiple uncorrelated strategies is one of the most effective ways to reduce portfolio volatility. AlgoCloud supports multiple strategies running simultaneously with separate position sizing.

How much capital do I need?

There’s no fixed minimum, but to properly diversify across 15–20 positions, most traders start with at least $10,000–$20,000. Alpaca, AlgoCloud’s default broker integration, has no account minimum.

What if the strategy has a losing year?

Every strategy does. Momentum had a significant crash in 2009. Mean reversion underperforms in strong directional trends. A bad year doesn’t mean the strategy is broken — it means it’s going through a normal cycle. The key is whether the long-term edge is still intact.

Do I need to monitor the strategy daily?

No. Once deployed, AlgoCloud runs the strategy automatically. It scans stocks, selects positions, and places orders on the schedule you set. You can check in weekly or monthly to review performance.

New to algo trading? Start with how to build your first stock picking algorithm — a step-by-step guide with no coding required.

Libor Štěpán

AlgoCloud trader

Related Articles

- Russell 1000: Buying Dips Strategy – Another mean-reversion approach applied to Russell 1000 stocks

- 7 Best Algorithmic Trading Platforms for Stock Picking (2026) – Compare platforms for running strategies like these

- Turn-of-the-Month Strategy with Volatility Filter – How regime filters improve trading performance