The original article appeared on AlgoHubb.com.

Understanding transaction costs in historical tests is an extremely important topic for every trader, especially short-term and algorithmic ones. Getting transaction costs wrong in your backtests can make a profitable-looking strategy fail completely in live trading.

What Transaction Costs Should I Assume in Historical Tests?

I first approached analyzing transaction costs in historical tests using Alpaca & AlgoCloud in mid-2024 with a sample of about 1,000 real transactions for the period 11.2023–07.2024.

In February 2025, I returned to analyze the costs again, this time with a sample of over 6,000 transactions on both Alpaca accounts (real and demo) for the period 11.2023–02.2025.

Now, I can answer with much greater confidence the crucial question: What are the real transaction costs when using Alpaca and AlgoCloud?

In the second part of this article, you will receive specific setting guidelines that I use in my backtests, but let’s start with what and how I investigated.

Objective and Method of the Transaction Cost Study

- The study aimed to determine the actual slippage and spread for market orders placed at the end of the day (ON BAR CLOSE). These orders are placed about 3–4 minutes before the market closes and are compared to the close prices recorded on daily candles used for backtesting.

- My study included 2,227 LONG transactions on a real account and 3,548 transactions on a demo account.

- I use the broker Alpaca, so I do not incur any commission costs except for REG/TAF fees, which are marginal (details in my trading costs article).

- I base my analysis on the closing transaction prices recorded in AlgoCloud (csv export). The sample concerns strategies operating on companies from the S&P 500 and Nasdaq 100 indices.

- I compared this “close” price to a reference source — the official Close price of that day, according to Nasdaq Financial Data. I used this source due to the unadjusted close.

Results: Real Transaction Costs in Historical Tests vs Live Trading

Here is a summary of the obtained results:

A screen of the Real account sheet. The full data can be found below.

Histogram showing the distribution of price differences based on Real account data. Positive difference = unfavorable. Negative = favorable.

Full research results are available in the Google Sheet.

How About Dividends in Transaction Cost Analysis?

To ensure accuracy over the long term, we need to use the unadjusted close — the actual price of the day without considering splits and dividends. If we don’t, the study might be too optimistic because the adjusted close tends to decrease over time, skewing the results.

However, this means the study doesn’t include dividends paid when holding a position on the Ex-Dividend Date. I view dividends as a bonus — like the cherry on top, reducing our transaction costs — but this is not included in the study.

Summary: What Transaction Costs to Expect in Historical Tests

The result obtained on the real account — 0.015% — is several times better than the 0.05%–0.1% I most often assumed in backtests.

Interestingly, the results from the real account are better than from the demo account, suggesting responsible simulation of order execution by Alpaca.

The timing used by AlgoCloud, which operates on bar close with about a 3-minute delay, is cost-effective.

While total transaction costs can be higher depending on how a position is opened, most of my strategies use Limit orders. This approach helps avoid the spread from the beginning.

In my opinion, we live in beautiful times because transaction costs have never been so low for individual investors!

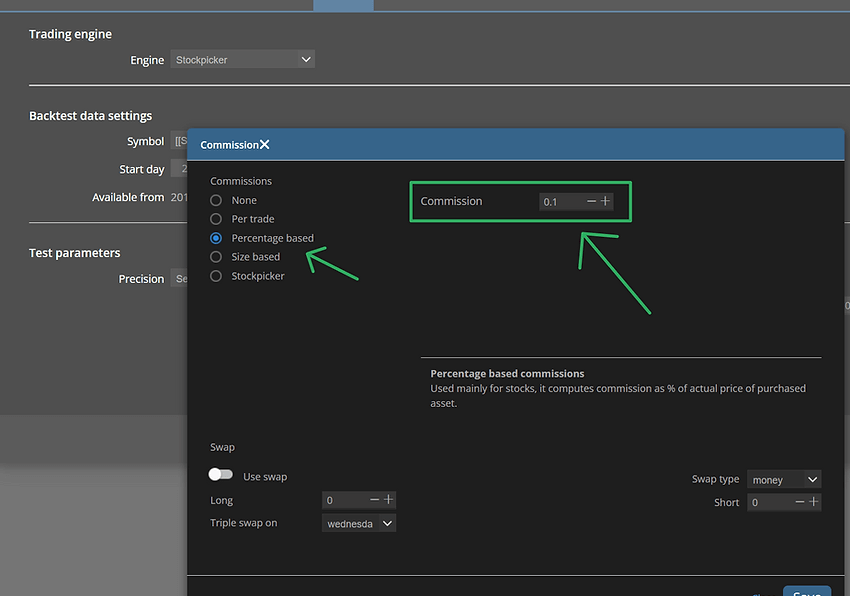

Safe Assumptions for Transaction Costs in Historical Tests

Here is my standard historical test setup with strategy settings:

Type 1: Entry – Limit / Exit – Market, On Bar Close

The costs we assume are 0.05%, which is over 3x more than what came out in the real account study (0.015%).

Type 2: Entry – Market On Bar Close / Exit – Market On Bar Close

The costs we assume in backtests are 0.1%, which is almost 7x more than what came out in the real account study.

In this case, slippage occurs 2x (on entry and exit), so it requires at least double consideration. I currently have too little data to assess the market order entries themselves, but I plan to expand my research in the future.

All strategy tests conducted at AlgoHubb have such or similar transaction cost settings during the strategy testing phase.